Death to AMMs? Next DEX Evolution

Liquidity is the blood that flows through the veins of every market. In the past, this was exclusively provided by market makers on centralized crypto exchanges until the Automated Market Maker (AMM) Uniswap model became the DeFi standard.

Although this was a massive first step for automatic permissionless trading, the end user experience was far from perfect. To this day, issues rarely seen in TradFi plague DeFi participants. However, a new model known as Proactive Market Making (PMM) is seeking to disrupt the industry.

In this article we will cover:

Why So Many Problems With Amms?

How Proactive Market Maker (PMMs) Work

Emerging Players

Potential Risks

Why So Many Problems With AMMs?

AMMs function through pre-funded liquidity pools. Deposit capital into a pool, become an LP, and earn passive income through accrued trading fees. Yet always remember to be prepared for impermanent loss, slippage, gas fees, multi-token exposure, and front-running.

Most DeFi participants are pretty aware of these, but why do they exist?

All these occur due to the linear arbitrage incentive model that AMMs run on. On constant product AMMs, every trade moves price away from the equilibrium liquidity that was initially deposited, which results in impermanent loss (IL). As price moves, arbitrageurs trade against stale prices, decreasing IL for LPs. Therefore, profit of LPs is a balancing game between earned trading fees and IL.

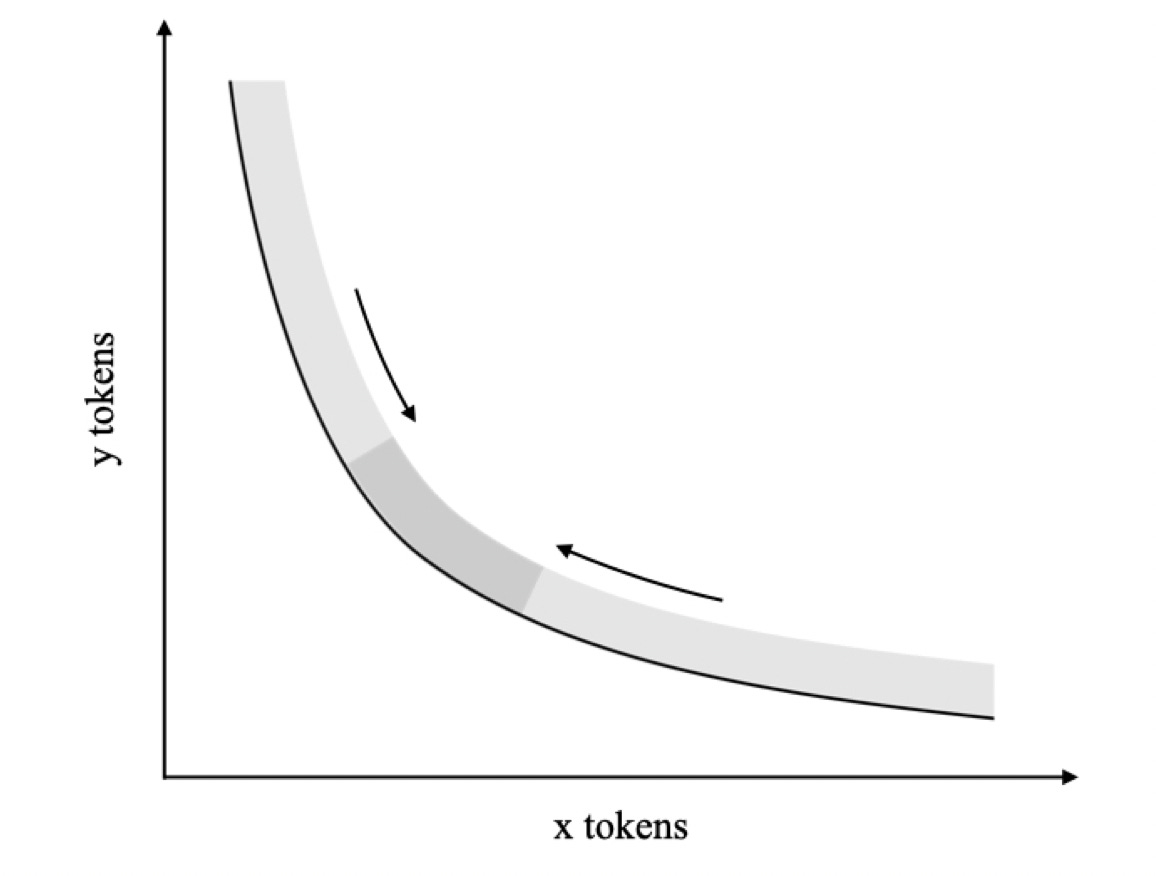

The linear models behind AMMs assumes the following that liquidity is distributed evenly across different prices; from zero to infinity.

We can easily see how this logic fails. Demand does not behave linearly in relation to price. Liquidity is usually accumulated around certain key levels that everyone watches.

Therefore, in AMMs, liquidity is allocated inefficiently and mostly lays dormant until a massive move occurs. This inefficiency in capital distribution also requires LPs to expose themselves to holding multiple assets in equal lots. Although permissionless, this can hardly compete with the centralized market maker model.

How Proactive Market Makers (PMMs) Work

PMMs attempt to anticipate market shifts and make adjustments in a non linear fashion. They account for the relationship between asset ratios, prices, order depth, etc. These new DEXs are able to generate much higher trading volumes at lower TVLs (Total Value Locked) while promising to create attractive LP incentives for their token holders.

For example, with a TVL of only $32m, Dodo DEX has done almost a billion dollars in 30 day trading volume. While Uniswap has seen $1.5b in volume and Sushiswap has had 232m, their TVLs are 3.1x and 3.6x larger than Dodo’s, respectively.

All of this is possible due to three main pillars that such decentralized exchanges are based on:

1 - Concentrated Liquidity

Concentrated liquidity improves capital efficiency for LPs while minimizing slippage for traders. It adds depth to a market by providing capital in a limited price range, thereby improving capital efficiency according to a modified coefficient pricing curve.

2 - Price Oracles

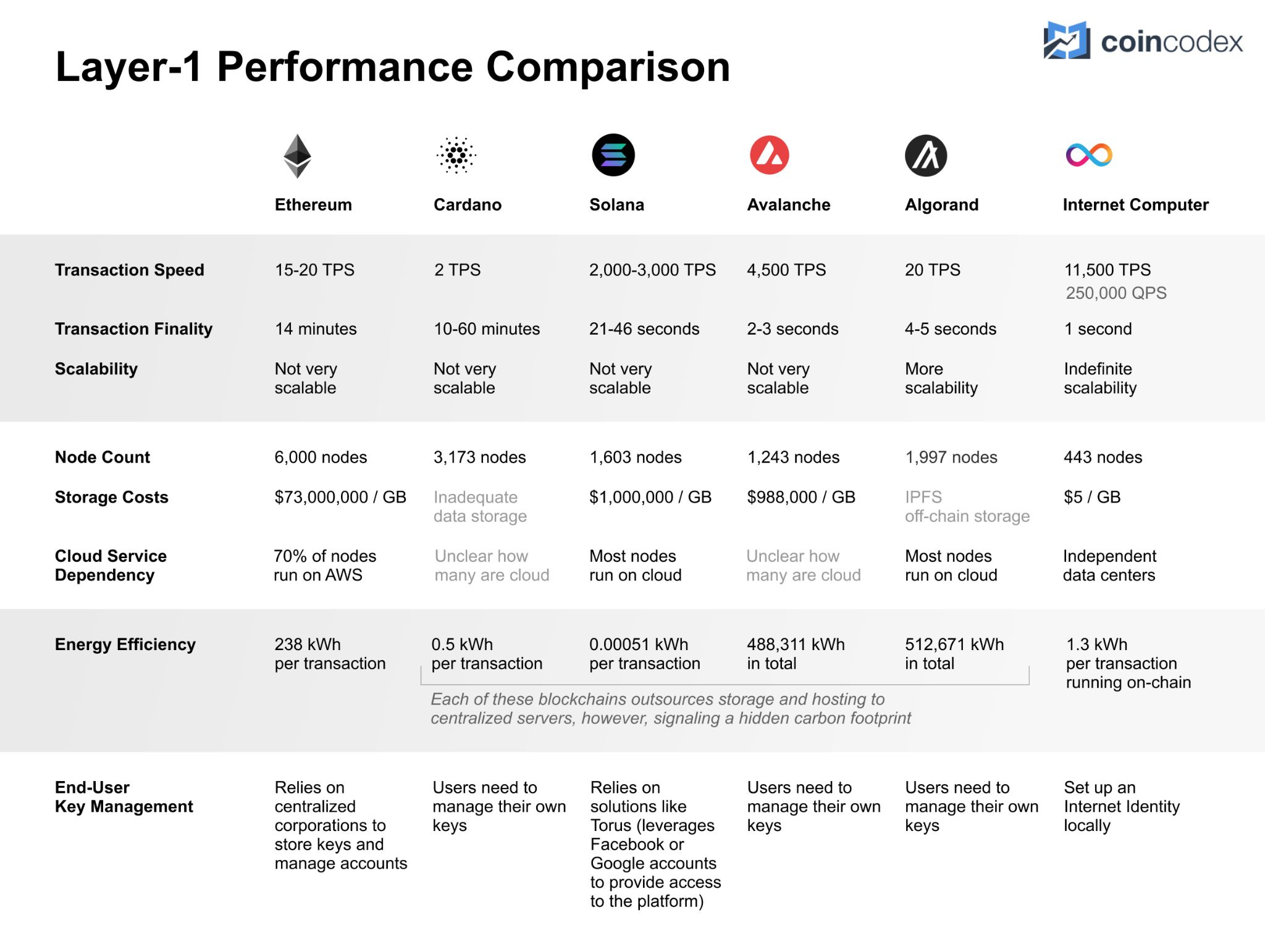

Oracles do not rely on arbitrageurs to adjust prices. Therefore, putting them onto blockchains with high TPS (transactions per second) not only makes PMMs like Lifinity $LFNTY) possible, but malicious actions like front-running highly improbable. While chains like ETH with 15 - 20 TPS may not quite work for this, others like Avalanche or Solana do the trick. This model helps Lifinity make more profit market making through sheer speed.

With this said, Dodo Exchange is on Ethereum. This is because they price their assets primarily based on the balance of assets in their pool and then use the oracle price to adjust it. Therefore, TPS isn’t as much of a priority here, but flexibility can still be maintained.

3 - Rebalancing Mechanisms

These ensure that pool balance regress to the pricing curve whenever a trade or price change occurs. Let’s consider the pool USDC / ETH. At any given time, PMM is in one of three possible states:

Equilibrium (ETH = USDC)

Base token shortage (USDC > ETH)

Quote token shortage (ETH < USDC).

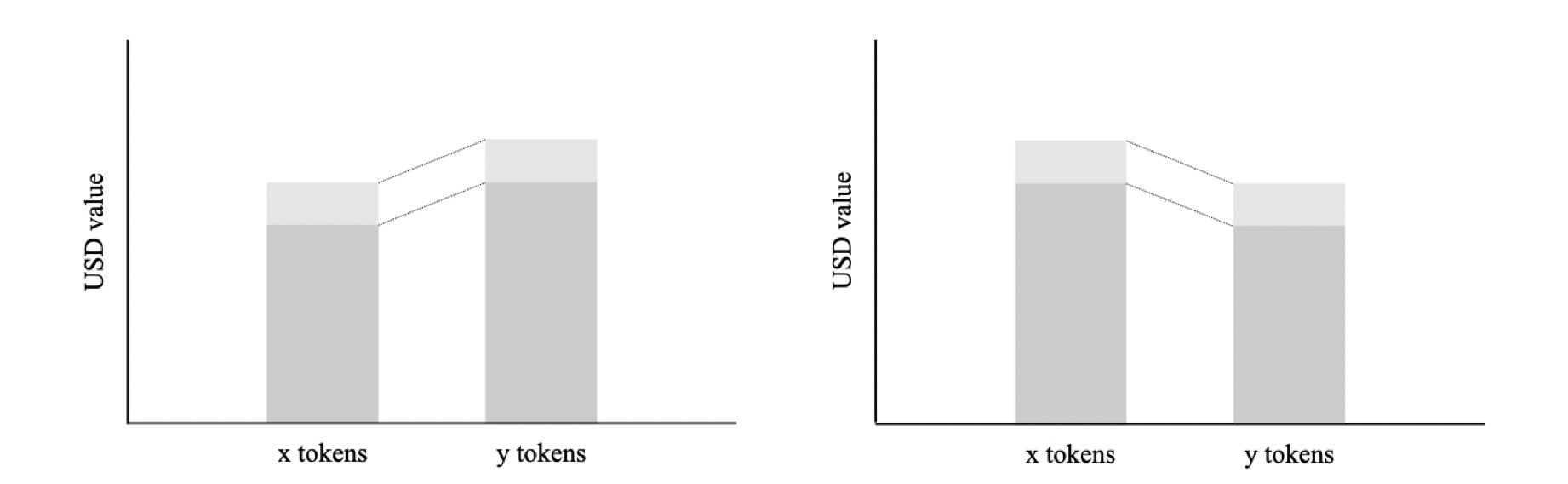

Prior to any transaction, the capital pool is in equilibrium. As the pool is used we end up with four possible scenarios where either the base or quote token is sold to make up the difference.

Let’s take a look at an FTM / USDC pool.

(1) ETH price rises - ETH makes up more than 50% of the pool

(2) ETH price falls - ETH makes up less than 50% of the pool

(3) ETH price rises - ETH comprises less than 50% of the pool

(4) ETH price falls - ETH makes up more than 50% of the pool

When a trader sells USDC, the FTM balance becomes higher than the USDC token regression target. In this state, the PMM will try to sell the excess FTM tokens in an attempt to decrease liquidity for buyers of FTM and increase liquidity for buyers of USDC.

In scenario 1 & 2, the LP would benefit and the pool would sell the excess for a profit.

In scenario 3 & 4, the LP would not benefit and liquidity would need to be adjusted.

This incentivizes traders to sell against the pool while discouraging them from buying, ensuring equilibrium is restored.

Emerging Players

Dodo Exchange ($DODO)

The first PMM of its kind that doubles as an aggregator and a DEX with various product offerings.

Fundamentals:

Built on Ethereum, hosted on Binance Smart Chain

Issuance / Infaltion Metrics

Tokenomics for V2

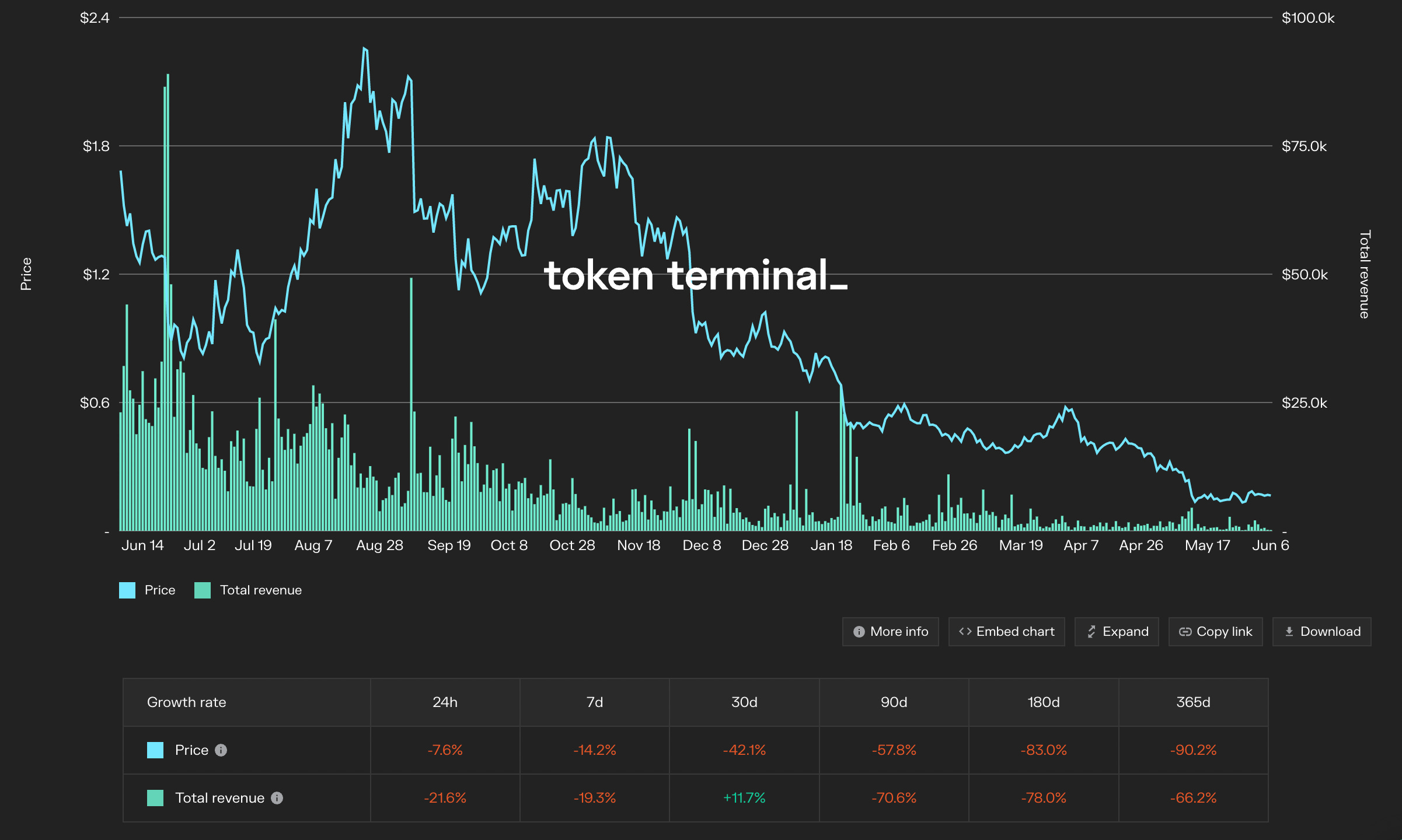

DODO runs on a membership / fee share based tokenomic model giving holders trading fee discounts and IDO participation allocations. Governance vDODO proof-of-membership tokens grants holders trading fee dividends and membership rewards, as well as the DODO holder benefits.DEX Trading Volume & Total Revenue has decreased this year, but that seems to be a result of the bear market versus anything exchange specific.

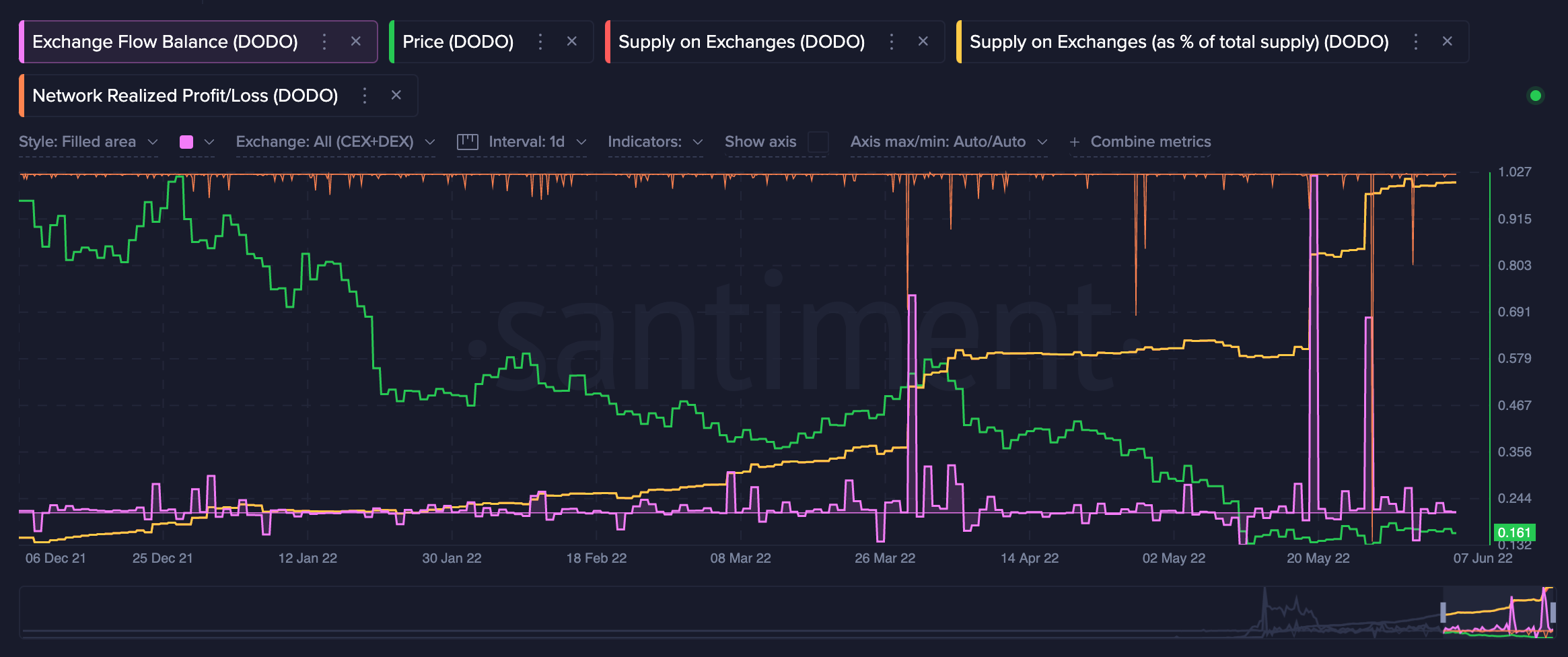

Blockchain Metrics ($DODO):

Supply on exchanges has risen significantly, at HODLers seemed to capitulate.

This can confirmed as capitulation since most of the coins were moved at a significant loss as evidenced by the “Network Realized P/L” metric.

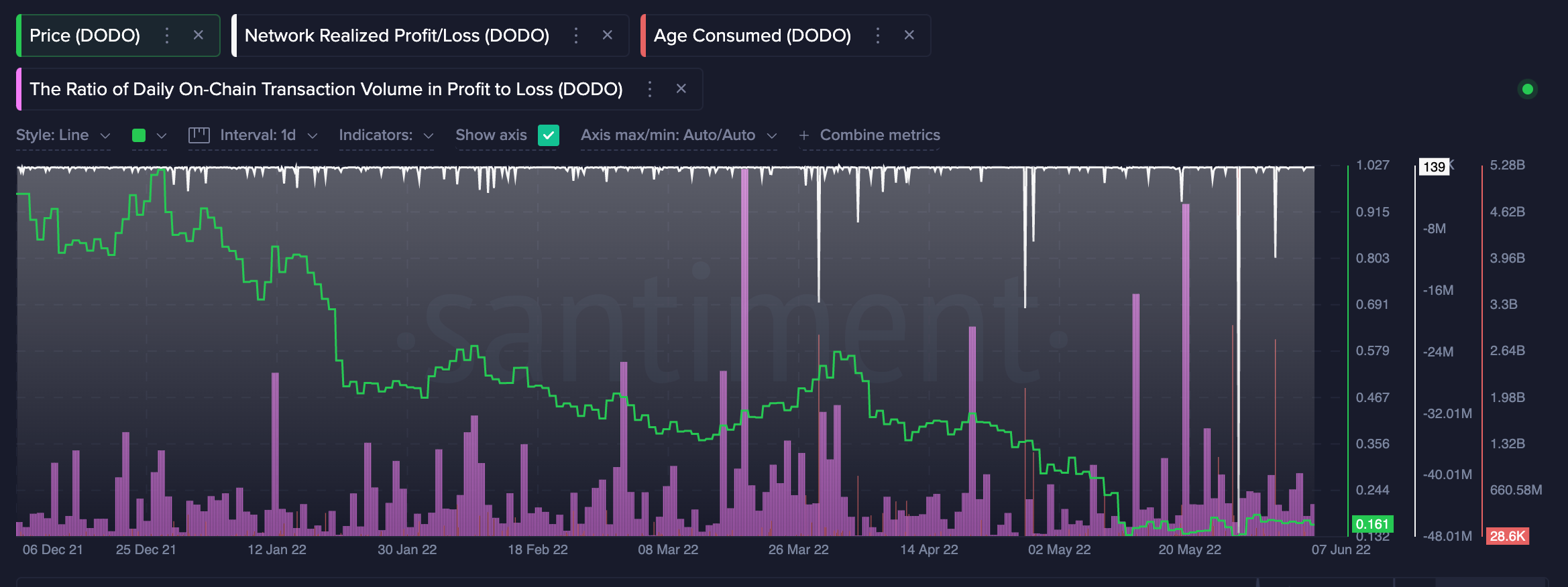

Daily active addresses have begun to grow once again, even after the massive spike in active deposits.

Futures Metrics:

Shorters were rewarded handsomely for quite a while, but looking at the overly negative predicted funding rates, with such high OI / Market cap ratio, squeezes were inevitable.

We can see the CVD (Cumulative Volume Delta) of stablecoin marginated contracts rise in tandem with these liquidations.

Spot:

Seems to be becoming a bit more interested in the token as well as shown by the green CVD above and we are seeing more a very high amount of buy volume coming in. Unless BTC pukes, there may be a case to be made for $DODO recovering.

Lifinity ($LFNTY)

Although a much younger player, and not as battle tested, they are definitely one to keep an eye on.

Fundamentals:

Blockchain: Solana

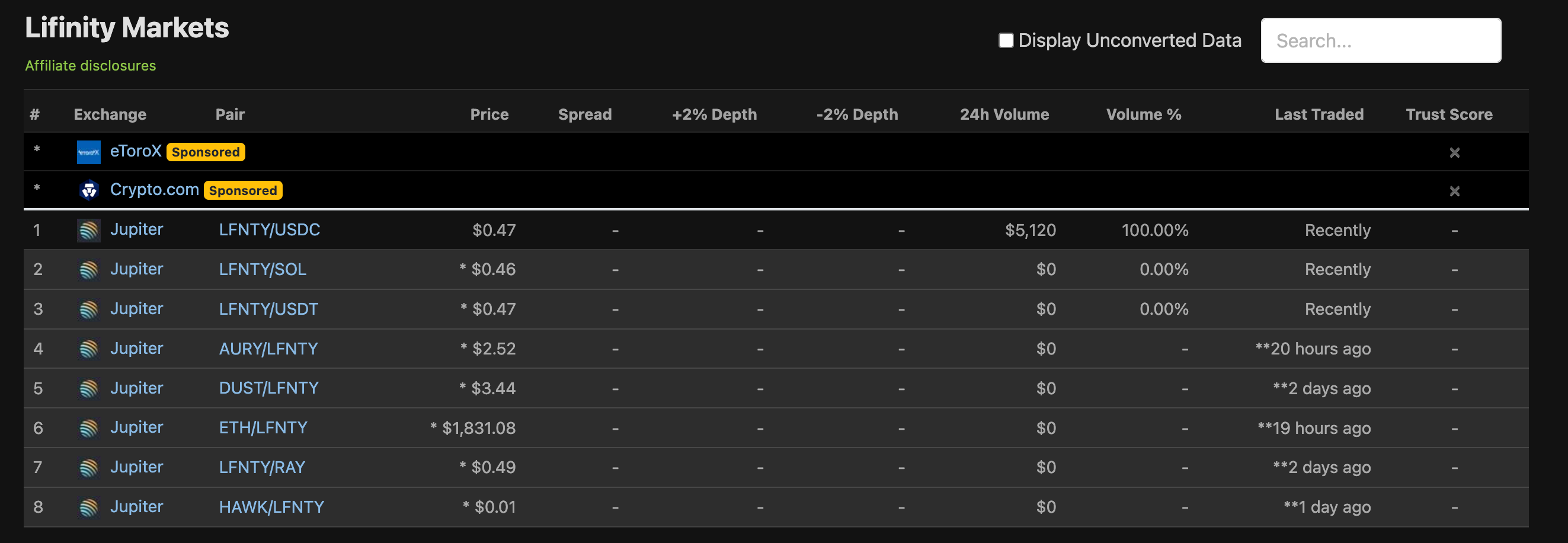

One exchange listing, little volume. However, the token has only been around for a little over a month as of the time of writing so no on-chain data or futures markets available.

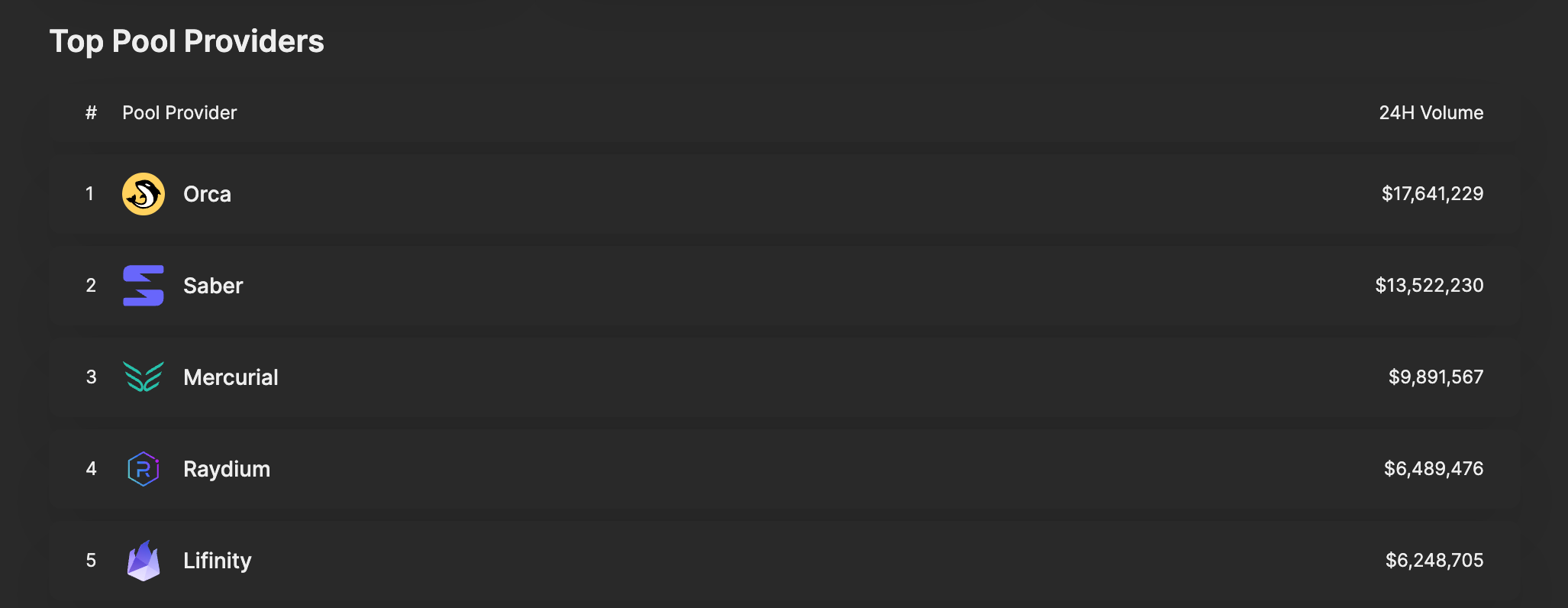

On Jupiter exchange, Lifinity is 5th out of 14 pool providers and has reached a billion in total volume.

Team: Anon

Top Investors:

The project had a capped raise and majority of the funds raised became protocol-owned liquidity used to generate trading fees and market making profit. Protocol revenue is distributed to veLFNTY holders, so token has a clear use case a relatively low maximum fully diluted valuation.

Tokenomics

Investors receive protocol revenue while LFNTY tokens are constantly being repurchased. Other protocols are happy because they are receiving subsidized liquidity while the LFNTY attains more protocol owned liquidity and more users.Users can lock up LFNTY for veLFNTY, which decays and unlocks linearly

Lifinity sells veLFNTY for LP tokens to permanently own the liquidity it provides

veLFNTY holders vote for the pools where LFNTY is sold as veLFNTY for LP tokens

Protocols can bribe veLFNTY holders to vote for emissions to be allocated to their pool

Revenue is distributed to veLFNTY holders and used for LFNTY buybacks

Security Audits — N/A

Risks

It seems that more and more advancements in the blockchain space are requiring off-chain solutions and this is no different. In the interest of speed, some of the work in a PPM system is done off-chain and then merged to the main chain. Furthermore, the reliance on oracles for pricing data creates a point of failure. This has happened multiple times in the past to various prominent blockchains like Solana and Luna. Whether due to a bugs of nefarious attacks, these are vulnerabilities that need to be addressed.

Ultimately, PMMs create a higher level of customization in an LPs strategy. Typically, LPs are short volatility and live in fear of sudden price shifts. With PMMs, they could engage in active price discovery through single asset deposit / withdrawals and utilize numerous market making strategies that limit oracle exposure.

Disclaimer: This content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.